Euroland since May 2012

Click here for a list of Eurozone countries in 2010 ranked by GDP

Click here for an article in June 2012 on Risk Weighted Assets within the Euro banking system

Click here for the background to the Libor scandal.

Click here for How much Greece owes to international creditors

Click here for prior news from May 4, 2010

Go to latest news as at August 21st, 2013

Greece teeters on the brink

The Australian

Peter Wilson, Europe correspondent

Friday, May 18th, 2012

THE ballot that Greece will hold on June 17 is not just a national election, it is also a referendum on whether Greece will stay in the euro, according to German Chancellor Angela Merkel.

Voters will choose between parties that are willing to abide by the austerity promises that Greece made in March in return for an international bailout, and more radical parties that are committed to rejecting austerity, which Merkel says will end the bailout funds and lead to default and Greece's exit from the 17-nation eurozone.

There are three possible outcomes of the election.

- Mainstream parties win; Greece stays in the euro (25 per cent probability)

THE next month will see a concerted effort by Greece's neighbours and lenders to convince voters that the leading anti-austerity parties are wrong when they claim Greece can reject austerity but still retain the euro. So far the left-wing party Syriza and other austerity opponents have managed to convince many voters that Europe would not dare to cut off bailout funds and force Greece out of the euro, for fear that the economic turmoil would spread to the rest of Europe.

"It's very difficult for them to throw us out of the eurozone," says Gabriel Sakellaridis, Syriza's economic co-ordinator. More than two-thirds of voters went for anti-austerity parties at the May 6 election, even though polls show three-quarters of voters want to keep the euro.

Syriza, which won 51 seats, has cast the election as a referendum on austerity but European leaders and the International Monetary Fund will join the leaders of Greece's traditional ruling parties (New Democracy and Pasok) in warning it is a referendum on the euro, not just austerity. Those two parties won 149 of the 300 seats in parliament on May 6 and if they lift their vote next time or lure the small Democrat Left party, which won 19 seats with 6.1 per cent of the vote, into a coalition government they will be guaranteed a sympathetic ear from a relieved Europe when requesting some softening of the austerity package.

- Anti-austerity parties do well and Europe backs down; Greece stays in the euro (20 per cent probability)

EVERY opinion poll conducted in Greece since the May 6 election has shown a rise in support for Syriza, which is tipped to become the largest party in the next poll. That would give Syriza the 50-seat bonus that the Greek system awards to the largest party, probably lifting it well above 120 seats. Even if the radical left party could not form a stable majority government it would certainly be big enough to stop the diminished centrist parties from forming a ruling coalition government.

The "mainstream" Pasok and New Democracy parties would be unable to enforce the spending cuts and other reforms needed to keep Greece's promises under its bailout agreements. Syriza insists it could renegotiate the €240 billion ($307.4bn) bailout packages that have led to average income cuts of more than 20 per cent in a little more than two years. German Foreign Minister Guido Westerwelle says the consequences would be inevitable as "the payment of further aid tranches won't be possible", but some European leaders would look for ways to avoid a Greek exit.

Going soft after such explicit statements from Germany and other countries would cost the EU enormous credibility and would be resisted by the IMF, which has also provided bailout funds and is rarely in a forgiving mood.

- Anti-austerity parties do well, Greece is forced out of the euro (55 per cent probability)

THE surge in support for Syriza detected by the polls could put it within striking distance of a parliamentary majority, and it may form a coalition government with the smaller Democrat Left or a temporary alliance with right-wing opponents of austerity. Even without forming its own ruling coalition Syriza could win enough seats to block a pro-austerity coalition, given the neo-Nazis and communists also took seats off the mainstream parties at the May 6 election.

A deadlocked result, like that on May 6, would leave the mainstream parties unable to take the austerity measures that are due as early as next month under Greece's bailout promises. Syriza knows most Greeks are desperately keen to retain EU membership, so there would probably be a blame-shifting game in which it tried to avoid jumping from the eurozone, instead daring the other 16 eurozone nations to expel it. But a crunch could not be avoided for long. Capital flight would start soon after an election victory for Syriza, which has vowed to stop Greece's loan repayments and break the "barbaric" austerity conditions imposed.

Reneging on loan repayments would led to default and Greece's banking system would be headed for collapse, with the European Central Bank and eurozone governments expected to withhold any significant rescue efforts. The Greek government and banks would be starved of funds, with the government forced to issue a new currency or short-term IOUs.

IF OPTION 3 PREVAILS …

How does a 'Grexit' work? how sudden would it be?

AN orderly change of currency, like Greece's entry to the euro in 2002, can be relatively smooth if transparent and carefully planned. That will not be the case in a Grexit. Even if the new government and European authorities were prepared to negotiate a staged departure, the issue would almost certainly be forced by runs on the banks and efforts by savers and businesses to get their euros out of Greek banks and, indeed, the country. The government would probably close businesses and banks for a holiday to reduce the disruption of the change.

It would rush to pass laws forcing the conversion of euro bank deposits into drachmas, and would impose limits on capital withdrawals and border controls to try to stop funds flowing to safer havens for euros. Manufacturers say it would take four months to print a new set of drachma notes and coins, and in the interim the government might be forced to use special stamps on euro notes.

There would be widespread confusion, as every business and individual tried to work out which mortgages, debts and contracts were denominated in euros and which were in the new drachma, which would quickly fall in value. The chaos could see the government unable to pay pensions and public employees' wages for some time, and massive trade disruption would send prices soaring and endanger supplies of food, medicine and other vital goods.

What happens to people's savings?

THE new drachma would plunge in value by something like 50 per cent, wiping out billions of dollars of wealth. The euro would not suddenly disappear from Greece, as many people would continue to use it in cash transactions to escape the weakness of the drachma. But with the government no longer having access to capital markets or other sources of euros it would be forced to pay pensions, wages and such like in drachma. Almost all of Greece's banks would collapse or be nationalised and loans would become much harder to find.

Would Greece have to leave the EU?

IT seems so. The only legal provision for leaving the eurozone and escaping some of Greece's legal commitments to its fellow euro members is to leave the 27-nation EU altogether. The option of exiting the EU was introduced in the Lisbon Treaty of 2007. A full exit would be a dreadful blow to most Greeks, who cherish their status as a developed European country as well as the life-changing benefits of EU membership such as the protection of EU laws, the receipt of development grants and freedom to trade, travel and work anywhere in the EU.

Greece could probably negotiate membership of the European Economic Area, which would give it access to the EU market alongside non-EU members Iceland, Liechtenstein and Norway. But leaving the EU would be painful as Greece's Balkan neighbour Croatia is about to sign up, leapfrogging Greece in the community of wealthy democracies.

Would Greece's economy improve under the drachma?

IN the short term the present poverty and distress of austerity would be worsened by the chaos of what International Monetary Fund chief Christine Lagarde says will be a "messy" exit. Athens would be banned from international capital markets for years. Argentina, which defaulted on loans in 2002, is still banned on international debt markets.

The massive devaluation of the drachma would eventually make Greece more competitive, turning the Greek isles into a massive bargain for foreign tourists and making Greek exports cheaper in foreign currencies. But it would take many years before Greek businesses and individuals fought their way through the problems of having woken up one day to find that foreign goods and many of their own debts were still denominated in euros but they were suddenly earning in limp drachmas.

Would other countries be forced out of the euro?

THAT is the biggest question for the eurozone.

While Greece is only 3 per cent of the eurozone economy a Grexit sets a dangerous precedent of a country leaving the eurozone and places a question mark over other vulnerable economies such as those of Portugal, Ireland, Spain and Italy. However much the EU will rush to express its faith in Portugal, many savers and businesses will move their euros out of that country's banks, and even heavily indebted Italy will find itself paying a higher risk premium to borrow money.

The EU and European Central Bank have already signalled that they would be determined to stop any contagion spreading from Greece, and if they can convincingly "ring fence" Portugal, the euro could end up being more stable without Greece. Ireland and Portugal have made considerable progress in implementing their bailout packages and repairing their public finances. The EU has used the past two years to add important safety measures to its banking structure, economic rules and financial "firewalls".

What would be the impact on the rest of the world?

THAT depends on the extent of the contagion within the eurozone and the weakening of European banks.

Banks across the continent would be forced to write off Greek debts and some of the pain would be passed on through the global banking system. Jan du Plessis, chief executive of mining group Rio Tinto, said last week a Greek exit "would destabilise the European economy to a significant extent". While Australian banks have little direct exposure to Greece, some analysts warn that a mishandled Grexit could spark a new global credit crunch.

European trade would also be disrupted by a crisis of confidence and the EU is our third largest trade partner, behind China and Japan and almost as big as Nos 4 and 5, the US and Korea, put together.

Best-case scenario?

AFTER months of disruption Greece restarts its banking system and uses the cheap drachma to start attracting more tourists, replacing imports with its own products and even gain exports. Austerity continues and even worsens but at least with the prospect of medium-term growth.

Worst-case scenario?

POVERTY and chaos leads to more unemployment, street violence and even civil war. A government of inexperienced hardline parties would be running the show, and it may try to print money and spend its way out of trouble. A broader disaster would be a spread of Greece's economic chaos to other EU countries.

FRANCE and Germany have crossed swords over how to spur growth in the debt-stricken eurozone at an EU summit tinged by plunging markets and the euro hitting a near two-year low. "We have to act straight away for growth," French President Francois Hollande insisted amid deepening worries over Greece's eurozone future and Spain's troubled banks. "Otherwise there will still be doubt on the markets".

"We have no time to waste," the freshly elected Socialist leader stressed at his first EU summit after a cost-conscious train ride from Paris.

German Chancellor Angela Merkel faced pressure to give ground on her hardline austerity doctrine as the European single currency fell to $1.2564 and London, Frankfurt and Paris stock exchanges each shed well over two percent. However, she rejected a call by Mr Hollande for eurobonds — jointly pooled eurozone debt — on the grounds they are "not a contribution to stimulating growth in the eurozone" and adding that such instruments ran contrary to EU treaties. Berlin fears eurobonds would only result in German taxpayers permanently underwriting the public finances of weaker eurozone economies.

In a German press interview appearing on Thursday, Ms Merkel's finance minister Wolfgang Schaeuble maintained that "the differences between ourselves and France are not so great." Mr Schaeuble said Mr Hollande wants more done to kickstart growth, but insisted that the French president "does not want to water down" a treaty obliging balanced budgets the Frenchman initially said he wanted to re-negotiate. "We're not talking about an easing of budgetary discipline," Mr Schaeuble insisted. A member of Mr Hollande's entourage said he was "floating ideas" but "not coming to Brussels with a Kalashnikov."

Non-euro Britain also flexed muscles, ruling out in advance other core ideas put forward by European Union officials and backed by Mr Hollande — including a tax on financial transactions. Home to three quarters of Europe's financial services industry, London vehemently rejects the tax.

Opening the dinner talks, EU president Herman Van Rompuy underlined the need to find "a strong will to compromise" with the risk of knock-on effects from a Greek eurozone exit exercising markets. After Germany's central bank said the picture in Athens ahead of June 17 elections was "highly alarming," leaders were expected to remind Greek voters that they expect Athens to honour a 237-billion-euro ($300 billion) bailout deal agreed in March. "I don't believe we can afford to allow this issue to be endlessly fudged or put off," said British Prime Minister David Cameron, notably urging the European Central Bank (ECB) to do more.

Treasury officials from the other 16 eurozone member states were told this week to "reflect" on what an exit would mean for their economies, a diplomat from one eurozone country told AFP. The Greek finance ministry in Athens "categorically" denied this was the case.

Contingency planning that diplomats called "commonsense" stems from arguably greater worries about Spain and Italy, after a report by Fitch Rating agency showed foreign investors had fled Spanish and Italian debt in huge numbers. Spanish Prime Minister Mariano Rajoy said Spain did not require the support of European rescue funds, saying there were "faster instruments" — an apparent allusion to the ECB which has previously bought government bonds in sell-on markets. Analysts see this as inevitable, with consultant Sony Kapoor warning that Spain otherwise "is headed towards needing a fully-fledged bailout."

Wednesday's talks were set to endorse a trial for 230 million euros in seed money from the EU's budget this year and next by way of EU "project bonds." This is intended to attract 4.5 billion euros of long-term private investment for Europe's incomplete energy, transport and digital networks. Other ideas on the table included a 10-billion-euro boost to European Investment Bank (EIB).

THE lack of conditions attached to the €100 billion ($126bn) bailout for Spain emboldened Greece and other debtor nations to demand better terms from Europe yesterday. Syriza, the far-left party that could win the re-run of the Greek election on Sunday, said the Spanish deal showed Europe was abandoning its policy of austerity.

"Developments in Spain have confirmed the position we have supported from the start. Namely, that the crisis is a Europe-wide problem and that the way it has been dealt with so far is socially destructive and completely ineffective," Alexis Tsipras, the party's leader, who could be the next prime minister, told the Avgi newspaper. "Two years ago the crisis was related to the supposed laziness and unproductiveness of the Greeks. After two years of failure of the bailout memorandum, there is a dramatic increase in the voices calling for a policy change so as not to crash the whole European economy."

Greek politicians from all parties interpreted the Spanish deal as a sign that Athens has scope to negotiate a better deal with the EU, particularly after the election of the Socialist Francois Hollande as President in France. "What happened in Spain has great impact on Greece … (the accord) shows that a safety net for the eurozone is being prepared," said Evangelos Venizelos, the leader of Pan-Hellenic Socialist Movement (Pasok) and a former finance minister. Antonis Samaras, the leader of the conservative New Democracy Party and Mr Tsipras's main rival in the election, said the Spanish bailout suggested Greece should renegotiate rather than make the radical break promised by Syriza. "Think. While a country like Spain negotiates, there are some people here who argue that we must break things with Europe and isolate Greece," Mr Samaras said.

The speed and size of the Spanish bailout was prompted in part by the fear that a Syriza victory in the Greek election would prompt a run on the country's banks that could spread to other countries. The agreement provides Spain, the eurozone's fourth-largest economy, with up to €100bn on the best terms offered to any of the so-called PIIGS — Portugal, Italy, Ireland, Greece and Spain. The loan comes without the strict conditions and tight supervision that were part of the bailouts given to Greece, Ireland and Portugal. Spain will not have to enter a formal IMF program requiring economy-wide structural reforms. Nor will it have to submit to regular oversight visits by the European Commission, the European Central Bank and the IMF.

The money, from one of the two eurozone rescue funds, will be used to bolster the country's banks. The only requirement is the restructuring of the troubled financial sector, which has been left with billions of euros of bad loans by the bursting of the Spanish property bubble. Spain is implementing its own austerity program under Prime Minister Mariano Rajoy. As a fellow conservative, Mr Rajoy is trusted more by German Chancellor Angela Merkel than other leaders in the Club Med countries.

The terms offered to Spain have opened a pandora's box with other PIIGS, suggesting they might seek to renegotiate with Europe. Italy, the only one of the PIIGS that has so far not received a bailout, could now find itself in the crosshairs of financial markets. Its Corriere della Sera newspaper said it was concern about possible contagion that prompted Prime Minister Mario Monti, who is also Finance Minister, to play a key role in negotiations leading up to the Spanish bank rescue. "Monti lobbied for Spain not to be lumbered with an austerity plan like the ones for Greece, Ireland and Portugal," it said.

MOODY'S Investors Service downgraded its rating on Spain to the brink of junk territory and placed its ratings on review for possible further downgrade, pointing to the country's plans to borrow up to 100 billion euros ($126.5 billion) from the European Financial Stability Facility (EFSF), the government's limited financial market access and continued weakness in the economy. Moody's lowered Spain's bond rating three notches to Baa3, placing it one level above junk territory, from A3.

The firm noted Spain's decision to seek up to €100 billion of external funding from the EFSF, or its successor the European Stability Mechanism (ESM), will materially worsen the government's debt position. Moody's now expects Spain's public debt ratio to rise to about 90 per cent of gross domestic product this year and to continue to rise until the middle of the decade. Additionally, Moody's noted the Spanish government's "very limited" financial market access is evidenced by the country's reliance on external funding from the EFSF or ESM and its growing dependence on its domestic banks as the primary purchasers of its new bond issues — which Moody's noted is an "unsustainable situation".

France, Germany cross swords over Eurozone growth

The Australian Online

AFP

Thursday, May 24th, 2012

Give us a better deal, says Greece

The Australian

James Bone, Athens, The Times

Tuesday, June 12th, 2012

Moody's downgrades Spain to near-junk status

The Australian Online

Nathalie Tadena, Dow Jones Newswires

Thursday, June 14th, 2012

|

Same Day

World braces for euro test as Greece heads for polls

Stephen Fidler, The Wall Street Journal

Additional reporting: Vanessa Mock, David Roman and Brian Blackstone

EUROPE, facing a momentous Greek election after a week of mounting financial stresses, is preparing for what some financial analysts are calling its 'Lehman moment': the prospect that Greece could leave the euro currency union following tomorrow's vote. Yet, European officials say that even an election that results in a Greek embrace of the euro and an acceptance of the terms of Europe's March bailout of the country may only temporarily ease pressure on the eurozone, whose crisis-management strategy many analysts say lies in shreds.

Borrowing costs in Spain and Italy rose sharply higher in recent days despite efforts to insulate Spain, the eurozone's fourth-largest economy, from the effects of Greek uncertainty by lining up a bailout request last weekend for as much as €100 billion ($125.4 billion) to boost the capital of Spanish banks. "We are back in the danger zone," said Jean Pisani-Ferry, director of Bruegel, a Brussels-based economic think tank.

Financial markets rallied modestly yesterday after unofficial Greek polls suggested the pro-European New Democracy party would claim victory in the national parliamentary elections tomorrow. Officials expect a government led by the party wouldn't insist on a radical renegotiation of the terms of the bailout. With a two-week blackout on polls, investors have little new data to help them guess whether Greek voters will support New Democracy or its rival, radical leftist Syriza party, which has insisted it would stick with the euro but rejects the bailout agreement.

Underlining Greece's economic challenges, Europe's biggest retailer, Carrefour, said yesterday that it was pulling out of Greece by selling its stake in a supermarket joint venture to its local partner, becoming the latest and largest company to get out of the struggling country.

While senior European officials insisted they didn't anticipate a sudden Greek exit from the euro, major central banks have lined up measures to calm markets in case the election result unsettles markets and further depresses growth. Yesterday, the European Central Bank president Mario Draghi, in an effort to calm investors, said that the ECB "will continue to supply liquidity to solvent banks where needed", adding to the more than €1 trillion in three-year loans it provided to banks in December and February. The US Federal Reserve has prepared contingencies, while the Bank of England announced plans on Thursday to insulate the UK if the euro crisis deepens. China has made preparations for the worst scenario in the eurozone crisis, Chen Yulu, an academic adviser to China's central bank, said today, by introducing policies to stabilise investment demand and gradually stimulate domestic.

German Chancellor Angela Merkel delayed her departure to a summit of the Group of 20 that starts on Monday in Mexico, a possible indication of nervousness over the outcome of the elections. Germany, the EU's most powerful economy, continued to signal it isn't inclined toward leniency with Greece. "Europe will not survive if we do not show enough solidarity, but it won't survive either if too much solidarity is shown," foreign minister Guido Westerwelle said yesterday.

Mr Westerwelle also made a distinction between Greece and other struggling eurozone members such as Portugal and Spain. "We have to recognise that the situation is very different across Europe," he told journalists in Berlin. The hardline message was repeated by German economics minister Philipp Roesler. In comments to appear tomorrow in German newspaper Bild, Mr Roesler said that there would be no renegotiation on Greece's aid package, as suggested by Greek political parties. "A material easing of the austerity measures won't be do-able," Bild quotes Mr Roesler as saying in a release publicising the interview. Any effort to overhaul the March bailout with Greece would severely test the willingness of eurozone paymaster Germany to provide more finance, increasing the risks of Greece departing the currency bloc.

While some officials, notably at the German Bundesbank, have said a Greek exit would be manageable, many analysts have said it could generate panic similar to the decision to allow the US brokerage house, Lehman Brothers, to fail in 2008. If one country can exit the eurozone, it will be clearer that other weak economies can also. Citigroup says it rates the probability of Greece's exit from the euro at 50 per cent to 75 per cent. If an exit is averted, Greece still will likely need more bailout aid in coming months to keep its economy limping along, and tensions between Athens and its official lenders are likely to return whoever runs the government. "Whatever the outcome of these elections, it will be very difficult for Greece to fulfil the requirements of its [bailout] program," Mr Michels said.

Even if Greece stays in the euro, pressure on Spain and Italy is unlikely to lift. The governments of both countries have relied heavily on foreign investors, and are now vulnerable because foreigners have retreated. The failure of last weekend's announcement of the preparation of a bailout plan for Spanish banks also exposed serious weaknesses in the region's rescue measures. The bailout funds can't directly provide capital to banks; they can only lend to national governments in order to give them the resources to bailout banks, swelling the debt burden of struggling governments.

The International Monetary Fund said yesterday that Spain must redouble its efforts to stop its debt from rising further. Spain's public debt rose to 72.1 per cent of gross domestic product, government figures released yesterday showed. That is 30 percentage points higher than in 2008. In another weakness of the bailout arrangements, the bailout loans will have a senior status, meaning that buyers of government bonds will move a notch lower in the pecking order in case Spain needs to restructure its debt. More than that, the funds aren't large enough to take over responsibility for the borrowing needs of Spain and Italy.

Flaws have also been exposed in the eurozone's other rescue plans. The ECB took no losses on its holdings of Greek government bonds when Greece restructured its debt earlier this year, subordinating government bondholders. A big ECB move to prop up Spanish or Italian bond prices would likely heighten worries of private bond investors that their interests will be muscled aside by powerful official creditors.

Beyond that, ECB moves to flood banks with long-term funding in December and February helped banks, but offered only short-lived support to government bond markets. That suggests another dose wouldn't resolve the fundamental underlying problems. Bank of England governor Mervyn King said on Thursday that the fact the boost from the ECB's long-term refinancing operations was so short-lived shows that a shortage of short-term liquidity isn't the eurozone's problem. "The problem is one of solvency," he said.

Given these weaknesses, financial markets appear to be seeking evidence that more decisive steps are being considered. These would entail the stronger governments taking some responsibility for the obligations of weaker governments and of troubled national banking systems. "The traditional instruments have reached their limit," said Mr Pisani-Ferry. "That's why people are starting to consider debt mutualisation and the issue of a banking union."

There is strong resistance to these concepts from the countries that are members of what some analysts have described as the 'Club of No': Germany, the largest European economy, backed by Finland, the Netherlands and Austria. The latest setbacks have further increased the pressure on Germany, whose chancellor, Ms Merkel, is likely to be pushed by other leaders at the G20 summit to take further steps to boost confidence.

Investors increasingly see two opposing outcomes from the crisis: an unravelling of the eurozone or decisive action from Berlin. If the euro is to be saved, many say, Germany or the ECB, and probably both, will have to put their resources on the line in a decisive way. That decision will likely be brought forward if an anti-austerity government takes power in Greece. In coming days, Berlin will have another decision to make, say European officials: to decide whether a new government in Greece is a partner that deserves further help or an obstructionist administration that should be left to go its own way.

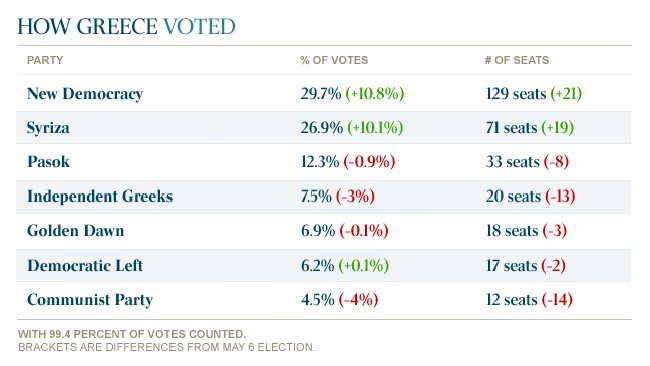

GREECE sent a sigh of relief through governments and financial markets around the world this morning by giving a narrow election victory to a party willing to stick to the country's economic bail-out agreements and defend the euro common currency. Antonis Samaras, the leader of the centre-right New Democracy beat off a challenge by the radical anti-austerity party Syriza and immediately promised that Greece would honour its commitments to pay off its debts and restore its public finances. "I am relieved," Mr Samaras said, after fears that the election of anti-austerity forces could have sent Greece crashing out of the euro. "I am relieved for Greece and Europe. As soon as possible we will form a government."

The German Government immediately signalled a willingness to soften the timing of Greece's loan repayments and the harsh austerity commitments under its 240 billion euro bail-out agreements with the European Union and IMF.

With 99 per cent of votes counted New Democracy had edged out Syriza with a lead of 29.7 per cent to 26.9 percent. The former ruling party Pasok , which also supported the austerity package, held 12.3 per cent to form a pro-austerity majority with New Democracy of 162 seats in the 300-seat parliament. New Democracy's slight lead over Syriza was crucial because the Greek election system awards a bonus of 50 extra seats in parliament to the party that comes first, so the New Democracy's lead of less than three percentage points translated into a massive parliamentary lead of 129 seats compared to Syriza's 71.

It is not clear exactly what sort of coalition government will emerge in the next few days but German Foreign Minister Guido Westerwelle said there was room for easing some of the harsh conditions of the bail-out agreement, which has sent unemployment soaring to 22 per cent by cutting public spending and raising taxes. "There can't be substantial changes to the agreements but I can imagine that we would talk about the time axes once again," he said. "But there is no way out of the reforms. Greece must stick to what has been agreed. If we said to Greece, no matter what we agreed, it doesn't matter anymore, then we would get a problem with all the other European countries that are diligently and persistently implementing their reforms."

With Greece's economy remaining in deep trouble the challenge facing Mr Samaras was shown by the fact that 52 per cent of voters continued to support the five anti-austerity parties which entered parliament. After weeks of warnings from European leaders and Mr Samaras that Greece faced catastrophe if it abandoned the eurozone the total support for New Democracy and Pasok, the only two parties which supported the bail-out agreement, rose from 32.1 per cent in the May 6 election to 42 per cent. The combined 13-seat gain of the two pro-austerity parties came at the expense of the two most extreme parties, the Communists (down 14 seats) and the neo-Nazi Golden Dawn (down three) while the three more mainstream anti-austerity parties gained four seats for a combined total of 108.

Mr Samaras said he wanted to form a broad "government of national salvation", and promised there would be no more of the anti-austerity "adventures" in Athens that had threatened the stability of the euro and raised fears of undermining other vulnerable countries such as Spain and sparking a world-wide credit crunch. "Today the Greek people expressed their will to stay anchored within the euro, remain an integral part of the eurozone and honour the country's commitments and foster growth," Mr Samaras said. "This is a victory for all Europe. I call upon all political parties that share those objectives to join forces and form a stable new government. I will make sure that the sacrifices of the Greek people will bring the country back to prosperity, we will work together with our partners in Europe in order to supplement the current (austerity) policy mix with growth enhancement policies. We are determined to do what it takes and do it fast."

Syriza leader Alexis Tsipras immediately ruled out joining any governing coalition while Pasok, the diminished giant of the centre-left, said it would not join any coalition that did not involve Syriza. Tough coalition bargaining will follow in the next few days but even if those talks fail New Democracy will be able to form a minority government and rule with the consent of Pasok.

The election confirmed a once in a generation political realignment with the eclipsing of Pasok by the more radical left-wing party Syriza as a major new political force. Syriza polled as little as 4.6 percent in 2009 and first overtook Pasok in a first national election on May 6 that ended with inconclusive coalition talks. The election saw a crash in the support of the hardline Communist Party, which almost halved its May 6 vote as left-wing supporters migrated to Syriza. The communists were on 4.5 per cent of the vote, down from 8.5 per cent on May 6 with their parliamentary presence shaved from 26 to 12.

In a development that will worry many European governments struggling with economic difficulties and rising immigration tensions the neo-Nazi party Golden Dawn consolidated its position, once again winning just under 7 percent of the vote and holding 18 of the 21 seats it won when it broke through on May 6 to enter parliament for the first time. A minor Left-wing party, the Democratic Left won 6.2 per cent for 17 seats and was quickly targeted by New Democracy as a potential coalition partner because of Mr Samaras's desire to build as broad a front as possible to share the political burden of tackling Greece's continuing spending cuts and tax rises.

Mr Tsipras, the 37-year-old leader of Syriza, said that instead of joining a broad coalition his party would fight on as an Opposition party to try to stop the austerity package, "and use our position for the benefit of the Greek people. We must all know that the austerity measures cannot go ahead because they lack the necessary legal basis. All parties have been forced to admit that the bailout deal is not a viable plan and this is clear from the Greek people's vote and the government that will be formed by New Democracy must keep in mind that when it comes to important issues they cannot proceed without taking into account the will of the Greek people. We will continue our struggle on Monday because we know that the future is not for those who are in fear but for those who carry on hoping."

European Union chiefs Herman Van Rompuy and Jose Manuel Barroso welcomed the result, saying they hoped to see the quick formation of a government to end the persistent uncertainty in Athens. "Today, we salute the courage and resilience of the Greek citizens, fully aware of the sacrifices which are demanded from them to redress the Greek economy and build new, sustainable growth for the country," they said in a joint statement. "We will continue to stand by Greece as a member of the EU family and of the euro area."

Minor parties which failed to reach the 3 per cent threshold required to enter parliament saw their vote crash from 19 per cent six weeks ago to just 6 per cent as votes consolidated around the leading parties.

Source:The Australian

GREECE'S largest political party made a crucial breakthrough in coalition talks this morning as world leaders piled pressure on Athens to form the broadest possible coalition to implement a gruelling austerity program. New Democracy, the centre-right party which topped Sunday's tightly-fought national election won an informal agreement from its traditional socialist rival Pasok to join "a government of national salvation" and will press on today to try to lure a smaller third party into its Cabinet.

New Democracy leader Antonis Samaras said his new Cabinet would make the hard decisions necessary to repay Greece's debts to the IMF and European Union but indicated that he would ask to have the target dates for 11 billion euro of additional spending cuts and tax rises pushed out to four years instead of two years. Analysts said that delay could require 16 billion euro of extra funding, requiring extra patience and funding from countries such as Germany. "We will have to make some necessary amendments to the bailout agreement, in order to relieve the people of crippling unemployment and huge hardships," Mr Samaras said.

LOS CABOS, Mexico: World leaders papered over their differences after clashing over the eurozone debt turmoil, deferring concrete decisions to other meetings amid worries about another global crisis. The Group of 20 advanced and developing economies pushed European nations to integrate banking systems quickly to calm the financial turbulence hitting Spain and threatening to ricochet around the world.

But the gathering, which ended yesterday, produced no acceleration in the timeline for financial integration, such as guaranteeing bank deposits across the 17-nation currency union. European leaders meet next week to discuss their road map, which could take years to implement.

The leaders floated a number of ideas for deploying the eurozone's rescue fund in different ways to control mounting threats to Italy and Spain. One idea: using the rescue money to tame borrowing costs for the two countries by buying sovereign debt, as an alternative to a traditional rescue program. While some European leaders said the idea was worth exploring, it faced tall hurdles to overcome political constraints. "The idea is to stabilize borrowing costs, especially for countries who are complying with their reform agendas, and this should be sharply distinguished from the idea of a bailout," Italian Prime Minister Mario Monti said.

The G20 leaders, whose nations represent about 85 per cent of global economic output, appeared to recognize the need for urgent action. But they found themselves with few options as they awaited action from Europeans. "We will act together to strengthen recovery and address financial market tensions," the leaders said in their joint statement.

Tensions between leaders mounted throughout the meetings in the Mexican coastal resort. As many from outside Europe pressed for swifter action, some eurozone officials grew defensive and maintained they were moving with urgency to overcome long-standing structural problems in their currency union.

The rift exposed a dilemma for the G20 in its seventh gathering of world leaders since the US financial crisis struck and dragged down the global economy. With just four of the eurozone's 17 nations attending the Mexico summit, European leaders sought to defer any major commitments until next week's meeting in Brussels. They pushed back against the notion that the 27-nation European Union could not solve the crisis on its own.

At the same time, European officials welcomed an expansion of resources at the International Monetary Fund, the world's emergency lender. The fund said it had received about $US456 billion of commitments, including the latest additions at the summit of $US43 billion from China and $US10 billion each from Brazil, Russia and India. The new pool of money nearly doubles the IMF's available lending capacity to about $US700 billion.

Many officials had warned in advance that concrete decisions about the eurozone would need to wait until next week's European summit. But after the G20, they said the latest talks helped guide that agenda by having European officials commit to strong measures to break the cycle of trouble between European governments and their banks. "They understand the stakes," US President Barack Obama said of European leaders. "And I'm confident that they can meet this test."

The stakes could not be higher for Mr Obama, who is running for re-election in a campaign focused on his stewardship of the world's largest economy. Americans already give him poor marks for his handling of the economy. A spread of the crisis in Europe, which Mr Obama says is already harming the US, would further hurt his chances of winning in November.

ATHENS: Greece's coalition government breezed through a confidence vote yesterday, winning the tough mandate of tackling a two-year-old crisis and keeping the country safely in the eurozone. The largely symbolic vote came as the French and German leaders sought to put aside squabbles over the eurozone before finance ministers met overnight to find ways to ease the debt crisis.

After three days of tense parliamentary debate, 179 legislators out of the Greek chamber's 300 voted in favour of a centrist coalition led by conservative Prime Minister Antonis Samaras that has promised to ease austerity measures while still meeting demands of EU-IMF creditors. The outcome of the vote was never really in doubt and aligned exactly with the 179 seats held by the Samaras-led coalition that unites his conservative New Democracy party with the socialist PASOK and the much smaller Democratic Left.

"You have followed the decisions of a three-party government that wants to proceed with reforms and change the country needs," Mr Samaras told deputies minutes before the vote. "We must stay in the euro according to the verdict of the Greek people."

The Samaras cabinet must immediately tackle the mammoth task of turning crisis-wracked Greece around while keeping the trust of EU-IMF creditors who hold the power to keep the country's finances afloat. The government said its first goal, along with carrying through a raft of reforms and privatisations, would be to secure an extension to the budget deadlines set out in Greece's €130 billion ($156 bn) bailout plan.

But Greece's new finance minister warned legislators that winning any kind of reprieve from lenders will not be easy as EU and IMF officials have shown stiff resistance to any talk of renegotiation, especially one that comes with a price tag. Finance Minister Yannis Stournaras said: "We will propose an extension of the deadline beyond 2014, but the difficulty is that it requires additional financing and therefore a consensus" (in Europe). "Greece has received until now the most aid ever given a country."

Hours earlier, Chancellor Angela Merkel and President Francois Hollande kissed and hinted that they might make up at a ceremony in Reims, eastern France, to mark 50 years of Franco-German friendship. But their love-in was marred by the revival of historic tensions after police said 51 German war graves had been desecrated at a nearby cemetery.

The complexities of the Franco-German relationship swirled around the windswept white stage. Mrs Merkel kissed the French President on both cheeks, for example, but only after she had insisted on the need for deeper political integration in Europe, about which France is distinctly wary. "We must complete economic and monetary union at a political level," she said. "It is a Herculean task, but Europe is capable of it."

THE International Monetary Fund is ready to pull the plug on Greece, forcing a bankruptcy as early as September, as the country's new Prime Minister said it is suffering a "Great Depression". Senior officials have told EU leaders in Brussels they are no longer willing to put more money at Greece's disposal, according to German newspaper Der Spiegel.

The IMF — part of the so-called troika monitoring Greece's compliance with bailout terms — is said to have concluded that the country will not succeed in reducing its debt to 120 per cent of gross domestic product by 2020. Giving Greece more time to meet its goals would require an additional €10 billion ($11.75bn) to €50bn in funding, on top of two previous bailouts, the report said, noting many Eurozone governments were not willing to shoulder new burdens for Greece. Some countries, such as the Netherlands and Finland, have made their support conditional on IMF participation.

The IMF, which traditionally is led by a European, has come under fire for being too soft on Eurozone countries. So far, it has helped to bail out Greece, Portugal and Ireland, while Cyprus has also requested support. The fund said yesterday: "The IMF is supporting Greece in overcoming its economic difficulties. An IMF mission will start discussions with the country's authorities on July 24 on how to bring Greece's economic program, which is supported by IMF financial assistance, back on track."

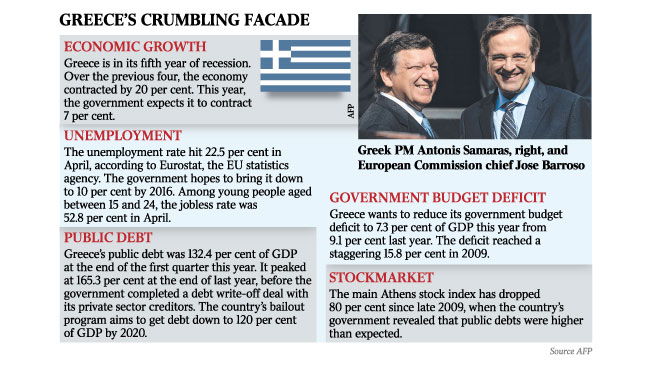

The new government in Athens is trying to find €11.7bn of cuts to meet the bailout target of cutting its deficit to under 3 per cent of GDP by the end of 2014, from 9.1 per cent last year and a peak of 15.8 per cent in 2009. The three-party coalition plans to ask the EU and the IMF to extend the 2014 deadline by two years. Greek Prime Minister Antonis Samaras compared Greece's predicament yesterday to what the US had endured in the 1930s. "You had the Great Depression in the United States," Mr Samaras told Bill Clinton, the former US president who was visiting Greece as part of a delegation of Greek-American businessmen. "This is exactly what we're going through in Greece. It's our version of the Great Depression."

A delegation from the troika — made up of the IMF, the European Commission and the European Central Bank — is due in Athens today to assess the country's efforts to meet agreed goals. Kathimerini, a Greek newspaper, reports the troika estimates a two-year extension will cost up to €40bn. Alexis Tsipras, Greece's leftist opposition leader, said at the weekend the country would default. He predicted that soon the government would present a return to the drachma as a national success.

German Economy Minister Philipp Roesler said he did not expect Greece to fulfil its requirements and that it would mean no more money to Athens. Der Spiegel suggested a formula would be found to tide Greece through August. The country faces the redemption of a €3.2bn bond before it is due to receive the next tranche of its bailout. The news weekly said fellow eurozone nations could not allow Greece to exit the euro before the new European Stability Mechanism was ready to prevent contagion. The mechanism cannot come into force until after a decision on September 12 by Germany's constitutional court.

Later same day 1:14pm THE EURO lurched towards the unknown yesterday as pressure on Spain, Italy and Greece reignited fears that the northern states lack the power or resolve to rescue the single currency. Madrid's funding costs jumped to record levels, with the yield on ten-year bonds reaching an unsustainable 7.55 per cent, the highest since the euro was launched in 1999. Stock markets slid as investors took fright at word that Spain's troubled regions were about to tap the state for their own bailouts.

Despite fierce government denials and a €100 billion ($118 billion) EU rescue for Spanish banks agreed last week, analysts believe that a full-scale bailout of the Spanish state may be imminent. That would use up all the resources of the bloc's new €500 billion permanent rescue fund — which cannot open at least until September because of legal challenges in Germany. "Events since Friday have been a clear wake-up call to anyone who thought that the Spanish bank rescue package had bought a calm summer for the euro crisis," said Carsten Brzeski, an analyst.

Pascal Lamy, Director-General of the World Trade Organisation, called the euro's predicament "difficult, very difficult". After meeting President Hollande in Paris, he said: "It is obviously the major challenge in the weeks and the months to come for the Europeans, but also for the rest of the world." In Britain, politicians were nervously watching the resurgent crisis and bracing themselves for further grim news. Figures due tomorrow are expected to show that GDP shrank 0.2 per cent in the April-to-June period, after a 0.3 per cent drop in the first quarter.

Spain, the eurozone's fourth-biggest economy, is at the heart of a flare-up that looks like a replay of last summer's alert when Greece, which is tiny in comparison, seemed close to dragging down the whole euro edifice. Italy, seen as the next domino if Spain falls, came under renewed pressure yesterday, with borrowing costs soaring. Italy's "spread" — the difference between local and German borrowing costs — touched levels not seen since shortly after Silvio Berlusconi's resignation as Prime Minister last autumn. The Milan stock market slumped and concern grew over the financial health of several Italian cities, including Naples and Palermo.

Mario Monti, the Prime Minister, brushed aside suggestions that the renewed emergency could force yet another special EU summit, only a month after the last grand attempt by EU leaders to settle the euro crisis. The "great nervousness on the markets doesn't have much to do with the specific problems of Italy", Mr Monti said on a visit to Russia. As stock markets fell across Europe, Madrid and Rome introduced temporary bans on short-selling, the practice in which traders bet on a fall in stock prices.

The International Monetary Fund attempted to quash reports, originating in the German media, that it was washing its hands of Greece after the latest €130 billion bailout, agreed in March, stalled, with Athens falling far behind in its commitments to reform. "The IMF is supporting Greece in overcoming its economic difficulties," a spokesman said, in response to reports that the IMF might refuse to contribute to an additional €50 billion it estimates may be needed by Greece.

Greek budget talks fail again, euro exit tipped GREEK leaders struggled to agree on required budget cuts yesterday as Citigroup raised the probability of the country's exit from the euro to 90 per cent. The leaders of the three parties in the new coalition government met for three hours to sign off on a plan for €11.7 billion ($13.7bn) in budget cuts demanded by Europe and the International Monetary Fund. However, the party leaders were unable to reach a consensus. The meeting ended shortly before talks began between Antonis Samaras, the Prime Minister, and Jose Manuel Barroso, the European Commission president.

Mr Samaras, who heads the conservative New Democracy party, will on Monday continue the talks with Evangelos Venizelos of the Panhellenic Socialist Movement and Fotis Kouvelis of the smaller Democratic Left.

After his meeting with Mr Samaras, Mr Barroso warned that Greece's new government must "deliver, deliver, deliver" on promises for cost-cutting reforms. "To maintain the trust of its European and international partners the delays must end. Words are not enough; actions are more important," he said.

Inspectors from the troika of the European Central Bank, European Commission and IMF met Yannis Stournaras, the new Greek Finance Minister, on Thursday and were to meet Mr Samaras yesterday. David Hawley, an IMF spokesman, said its mission in Greece was the first opportunity for "substantive" discussions with the new government. Those talks, he said, were expected to continue "into September". The troika's report will determine whether Europe and the IMF will release the next €31.5bn tranche of bailout funds to Greece, due in September.

The German news weekly Der Spiegel reported that Greece would not be allowed to default until after a German constitutional court hearing on September 12 on whether to permit the creation of the new European Stability Mechanism, which could be important in containing contagion from a Greek exit.

Citigroup economists said yesterday that chances of a Greek exit from the eurozone had risen to 90 per cent. The US bank also expects Italy and Spain to take a formal bailout on top of the banking aid of up to €100bn for which Madrid has already asked.

Citi said it expected further sovereign downgrades in the next two to three quarters with at least a one-notch downgrade by at least one leading agency for Austria, Belgium, France, Germany, Greece, Ireland, Italy, The Netherlands, Portugal and Spain.

ATHENS: Greece's leaders, struggling to reach consensus on an austerity program, will seek an extension of the country's bailout, a government official says, hoping to spread cuts of €11.5 billion ($13.4bn) over a longer time, even though international creditors have signalled this is unacceptable.

Prime Minister Antonis Samaras, Socialist leader Evangelos Venizelos and the leader of the small Democratic Left party, Fotis Kouvelis — the heads of the ruling coalition — met for more than two hours Monday but failed to reach a deal on the spending cuts Greece must enforce as part of a €173 bn bailout. This plan may already be off track after two election campaigns brought economic overhauls to a standstill.

"Discussions are continuing and will carry on in coming days," Mr Kouvelis said after the meeting. "We have in front of us specific issues, but we have a Greek society that cannot bear more burdens." The government official said Greece would push for a two-year extension to meet fiscal targets set out in its second bailout as it works to finalise the fresh austerity measures. The spending cuts and the extension of the program's timeframe "will happen in parallel," the official said.

The savings plan aims for cutbacks next year and 2014, as demanded by international creditors to keep funding lines to the country open. Without a green light from the troika — the European Commission, the International Monetary Fund and the European Central Bank — Greece may not receive its next €31 billion in funding, due to be disbursed next month.

Troika officials who arrived in Athens last week to review the delayed reform program have changed plans — they were due to leave yesterday but will now stay until the austerity measures are finalised. Greek finance officials said last week they have reached common ground with the troika on the parameters of the cutbacks, which could include further reductions in public-sector wages and pensions, although details have yet to be worked out. The new government is trying to convince international creditors it is serious about stepping up its reform program, which is months off schedule.

The economy, in its fifth year of recession, is expected to shrink more than 7 per cent this year, far worse than the European Commission's previous forecast of 4.7 per cent. This throws fresh doubts on whether Greece can achieve its debt-reduction targets and has raised concerns it may need another bailout or debt restructuring. "We all agree the road is difficult," said Finance Minister Yannis Stournaras. "Our choices must not nullify our ability to renegotiate and the country's ability to remain in the euro zone."

Reforms from privatisation of state-owned assets to liberalising the services sector, overhauling the tax system and curbing tax evasion were effectively put aside before the elections. To crack down on tax evasion, Greece yesterday asked the Swiss government to reintroduce a procedure allowing for the taxation of deposits held by Greek citizens in Swiss banks. According to some estimates, Greek residents hold as much as €200 billion in Swiss bank accounts.

THE troubled eurozone is on the verge of sliding into a double-dip recession for the first time after figures released yesterday showed that its economy shrank between April and June. The 17-nation region contracted by 0.2 per cent in the second quarter of the year after stagnating in the previous three months. The figure would have been even worse but for Germany's economy, which surprised analysts by growing by 0.3 per cent on the back of strong exports.

However, economists believe that Germany will struggle to drive growth in the region, with a barrage of recent gloomy data pointing towards a slowdown and even a contraction in Europe's powerhouse economy. Christoph Weil, an economist at Commerzbank, said: "An end of the eurozone recession is not in sight. On the contrary, the nosedive in the euro area actually appears to have accelerated in the summer. A fall in GDP now looks likely in Germany too in the third quarter."

German growth between April and June was driven by exports to countries outside Europe, such as China, but trade figures have shown a weakening in this trend in recent months. Also of concern for Angela Merkel, the German Chancellor, who has just returned from her summer holidays, is yesterday's closely watched ZEW index of investor sentiment, which slumped for the fourth month in a row in August.

France is also likely to face difficulties. Its economy has stagnated for the past three quarters and it has avoided recession only because it has not implemented harsh austerity measures. However, next month President Hollande has to find euros 33 billion (A$38.8 billion) in tax rises and savings for next year's budget.

Meanwhile, there was more pain in the peripheral nations in the second quarter of the year, with Portugal contracting 1.2 per cent, Italy by 0.7 per cent and Spain by 0.4 per cent. Another worry was that the economy of Finland, which is meant to be one of the stronger countries, shrank by 1 per cent.

Janet Henry, chief European economist at HSBC, said: "It is clear that the eurozone has moved back into a recession. This will make it even more difficult for most member states, not just those in the periphery, to meet their fiscal targets." This follows separate figures published this week, which showed that Greece suffered a 6.2 per cent annual drop in GDP in the second quarter of the year.

Tom Rogers, senior economic adviser to the Ernst & Young Eurozone Forecast, said: "The ECB's recent announcement that it will do 'whatever it takes' to save the euro is welcome, but clarity over what will be done is crucial."

EUROGROUP chief Jean-Claude Juncker has warned that Greece faced a "last chance" in proving its credibility to international creditors, saying the Greek government's proposal to extend overhauls would depend on the findings of a troika of inspectors expected to arrive in the capital of Athens next month.

Speaking after a meeting with Greek Prime Minister Antonis Samaras overnight, Mr Juncker also clearly declared his support for Greece's continued membership in the eurozone. "As regards the lengthening of the adjustment, I would say that this will depend on the findings of the troika mission," said Mr Juncker, who is also Luxembourg's premier. "I am totally opposed to the exit of Greece from the euro area," he added, saying Greece's departure from the common currency would pose a "major risk" for the eurozone.

His remarks came at the start of a week of high-level meetings between Mr Samaras and European leaders to discuss Greece's proposal to stretch out its overhauls. Tomorrow night Mr Samaras is due to meet with German Chancellor Angela Merkel in Berlin and, on Saturday, with French President Francois Hollande in Paris. In those meetings, he is expected to stress Greece's overhauls, while gently pressing for more time for budget cuts.

Greece's new government is proposing getting two more years to meet its deficit targets, without asking euro-zone partners for additional money. The request involves allowing Greece to spread painful cutbacks out to 2016 instead of to 2014, as stated in the existing agreement. If approved, Athens would be required to cut its budget deficit by 1.5 percentage points of gross domestic product annually, rather than the 2.5 points a year envisaged in the current plan.

The country's three-way coalition government — made up of the conservative New Democracy, socialist Pasok and small Democratic Left parties — hopes that giving Greece more time will ease the pain of the country's adjustment program, which has pushed the economy into a tailspin. "The only thing that Greece's government, its people and common sense is asking for, is to return to growth. Because an economy in a deep recession and massive unemployment cannot stand on its feet," Mr Samaras said. "And we are looking for a way for that to happen as soon as possible."

The troika — made up of representatives from the International Monetary Fund, the European Central Bank and the European Commission — is due to return to Athens in early September to assess Greece's efforts. A two-year extension would cost Greece's creditors at least €20 billion ($23.8 billion), according to Greek government officials. Countries such as Germany, Austria, Finland and the Netherlands all have repeatedly dismissed the notion of directly lending more money to Greece, so the proposal involves more indirect ways of financing that Athens hopes would be accepted.

The officials said Greece wants to use €8.2 billion conditionally earmarked by the IMF for Greece's use in 2015, and to cover the remainder by issuing more Treasury bills. The latter element would likely require reassurance from the ECB that it would continue to allow holders of the bills to refinance them either at its traditional credit windows or through Emergency Lending Assistance (ELA) from the Bank of Greece. The ECB stopped accepting Greek sovereign paper as collateral for its official lending facilities in July.

Under the new Greek plan, the government also will ask to push back the repayment period of its first EU-IMF bailout loan to 2020 from 2016. Athens used the issuance of Treasury bills this month to pay back a €3.2 billion bond maturity to the ECB. Greek banks used ELA to buy and refinance the bills.

The troika report is expected to be ready by the end of September, in time for an Oct. 8 meeting of euro-zone finance ministers that will decide on whether to disburse Greece's next EUR31 billion aid tranche, promised under terms of the country's bailout. But the ministers may also be forced to make tough decisions on the long-term prospects of Greece's aid program — beyond just deciding whether to grant a two-year extension.

A steadily worsening Greek recession, combined with government foot-dragging on promised privatisations and other economic overhauls, means it has become clear that Athens will need billions of euros of additional assistance only months after European leaders signed off on a fresh €173 billion bailout. If Athens doesn't get the money, the country could soon run out of cash, something that may force it to abandon the euro, an exit that could set off new turmoil in financial markets, dragging down other vulnerable southern European euro members, such as Spain and Italy.

Internal data from the IMF show that Greece's economy, already in its fifth year of a grinding recession, is sinking further. As a consequence, its debt burden — measured as a ratio to GDP — is climbing. The IMF now expects the Greek economy could contract around 7 per cent this year, 3.5 per cent in 2013, 1.5 per cent in 2014 and 0.5 per cent in 2015. That is far worse than the official, but dated, forecasts, made under the second bailout program in March, which sees Greece returning to growth in 2014. The new IMF forecasts mean that Greece won't meet a targeted 120 per cent-of-GDP debt ratio by 2020 — which would effectively force the IMF to halt any further funding for Greece.

The IMF has argued that Greece's debt must be reduced to "sustainable" levels — of around 100 per cent of GDP — before it releases any more aid to Athens. It thinks the most effective way to do this would be for Greece's euro-zone partners to forgive some of Greece's debt. The IMF has also put forward several options for filling the hole that will also lower Greece's debt ratio, but these ideas are meeting fierce resistance from the eurozone. The mildest would be another cut on the interest rate Greece must pay on loans from eurozone governments. The more-controversial options include having the ECB and euro-zone national central banks accept a rescheduling or a 30 per cent reduction in the value of their Greek bonds, said one official familiar with the discussions. Another scenario calls for euro-zone governments to accept haircuts on bilateral loans they made to Greece that could amount to well over €30 billion.

International inspectors have rejected parts of Greece's proposed austerity plan, forcing the country's coalition government to seek fresh spending cuts to meet creditors' demands. The inspectors rejected some €2 billion ($2.47 bn) of proposed spending and revenue measures the government had hoped would help meet budget targets for the next two years, Greek officials said. Party leaders from the three-way coalition — made up of the conservative New Democracy, socialist Pasok and Democratic Left parties — will meet Wednesday to try to find a compromise.

Fotis Kouvelis, the head of the coalition's junior partner, the Democratic Left, said after a meeting at the Prime Minister's office that "nothing has been decided" and said Greeks had reached the limits of their endurance with the austerity measures. Also on the weekend, Greece's finance minister and officials from the European Commission, the International Monetary Fund and the European Central Bank — the so-called troika — met to discuss the new measures, with all saying the meeting, which followed a month-long summer break, had been positive. But the troika and Greek finance ministry officials also emphasised that the talks were expected to last several weeks.

The troika is demanding €13.5bn in budget cuts in exchange for its latest €173bn bailout. They are the latest in a series of austerity measures Greece has taken over the past 2½ years to close a yawning budget deficit and that have driven the economy into a recessionary tailspin, sent unemployment to record highs and pushed the purchasing power of wage-earners down to levels not seen since 2003.

On the weekend, tens of thousands of demonstrators marched through the streets of the northern city of Thessaloniki, the first large-scale protest against the austerity measures, which foresee steep cuts in pensions, health-care spending and public workers' wages. Police said about 30,000 — 35,000 protesters took part in five marches called by unions and left-wing organisations.

EUROPE'S fragile financial calm was shattered yesterday, as investors worried that violent anti-austerity protests in Greece and Spain's debt troubles showed that the continent still cannot contain its financial crisis. Police fired teargas at rioters hurling gasoline bombs and chunks of marble during Greece's largest anti-austerity demonstration in six months. The protests were part of a 24-hour general strike, the latest test for Greece's coalition government and the new spending cuts it plans to push through.

The brief but intense clashes by several hundred rioters among the 60,000 people protesting in Athens came a day after anti-austerity protests rocked the Spanish capital.

In Madrid, thousands of angry protesters again swarmed as close as they could get to parliament yesterday, watched by a heavy contingent of riot police. There was no fresh violence, but the demonstrators cut off traffic on one of the city's major thoroughfares at the height of peak hour. The protesters chanted for the release of 34 people detained on Wednesday in clashes that injured 64 others. They also demanded new elections to oust Prime Minister Mariano Rajoy and his conservative government, which has imposed cutbacks and tax hikes, deepening the gloom in a country struggling with recession and unemployment of nearly 25 per cent, the highest among the 17 nations using the common euro currency.

Spain's central bank warned that the country's economy continues to shrink "significantly", sending the stock index tumbling and its borrowing costs rising. Across Europe, stockmarkets also fell and the euro was hit.

The turmoil ended weeks of relative calm and optimism among investors that Europe and eurozone might have turned a corner. Markets have been breathing easier since the European Central Bank said this month it would buy unlimited amounts of government bonds to help countries with their debts. The move by the ECB helped lower borrowing costs for indebted governments from levels that only two months ago threatened to bankrupt Spain and Italy. Stocks also rose. Media speculation about the timing and cost of a eurozone breakup or a departure by troubled Greece faded.

However, the economic reality in Europe remained dire. Several countries have had to impose harsh new spending cuts, tax rises and economic reforms to meet European deficit targets and, in Greece's case, to continue getting vital aid. The austerity has hit citizens with wage cuts and fewer services, and left their economies struggling through recessions as reduced government spending has undermined growth.

"Yesterday's anti-austerity protests in Madrid, together with today's 24-hour strike in Greece, are both reminders that rampant unemployment and a general collapse in living standards make people desperate and angry," said David Morrison, senior market strategist at GFT Markets. "There are growing concerns that the situation across the eurozone is set to take a turn for the worse."

Spain has struggled for months to convince investors it can handle its debts. The government is to unveil an austere 2013 draft budget and new economic reforms overnight. It has already introduced €65 billion ($80.bn) in austerity measures. Greece has been dependent since 2010 on billions of euros in rescue packages.

GREEK lawmakers have narrowly passed a crucial austerity bill by majority vote, but with heavy dissent from within the three-party governing coalition. Immediately after the vote early today and before the tally had been officially announced, two of the coalition parties expelled a total of seven dissenting deputies from their ranks. The third party in the coalition, the small Democratic Left, mostly voted "present" — in essence abstaining from the vote.

The passage of the bill was a big step for the government to secure continued funding from the country's international creditors. Without the loans, Prime Minister Antonis Samaras has said Greece would run out of euros on November 16. Last night, an anti-austerity demonstration by more than 80,000 people in Athens degenerated into violence as hundreds of protesters clashed with riot police before the vote.

The bill is the toughest test yet for the country's fragile four-month-old coalition government, which must pass the 13.5 billion euros ($16.5bn) package of measures to ensure Greece continues receiving bailout loans and avoids bankruptcy. "Today we must confirm Greece's new credibility," Mr Samaras said. "We choose whether we want to stay in the eurozone … or return to the drachma. That is the choice."

The measures will pile more pain on the Greeks, who have suffered wave after wave of spending cuts and tax hikes since their government revealed in 2009 that public debt was actually far higher than officially declared. Hundreds of rioters yesterday hurled rocks and gasoline bombs at lines of police guarding parliament, who responded with volleys of teargas and stun grenades, and the first use of water cannon in Greece in years. Some in the demonstration, which braved sometimes torrential rain, ran for cover as running battles broke out with police on the second day of a 48-hour general strike. Clouds of teargas rose from Syntagma Square.

The Prime Minister's website and another government site were also taken offline for more than an hour by denial-of-service attacks, presumably launched by a protest group, a state official said. The official, who was not authorised to make statement to the news media, asked not to be named.

"Today we face the most critical decision any government has taken in the past 37 years," Mr Samaras said. "Many of these measures are fair and should have been taken years ago, without anyone asking us to. Others are unfair — cutting wages and salaries — and there is no point in dressing this up as something else."

The alternative is bankruptcy, triggering financial chaos as the country would likely have to leave the 17-country euro bloc. "The alternative is much worse than any of these measures," Mr Samaras said.

Greece's next bailout loan instalment of 31.5bn euros, out of a total of 240bn euros, is already five months overdue. It is unlikely that Greece will receive the next bailout instalment in time for Mr Samaras' deadline next week. The payment was expected to be approved at a meeting of European finance ministers next Monday.

The 48-hour general strike against the bill shut down the public administration, left hospitals functioning on emergency staff and closed schools and tax offices. All ferry and train schedules were cancelled until today, flights were disrupted by a four-hour air traffic controllers' strike and Athens was without public transport for most of the day. The country's biggest union has also called for a demonstration on Sunday evening, when the 2013 state budget is due to be voted on.

GREECE'S international creditors reached a deal to end an impasse over the country's rescue program, though lingering differences over Greece's bailout signalled a lasting solution for the government's heavy debt burden had yet to be found. Finance ministers from the 17-country eurozone and the International Monetary Fund struck a deal in Brussels to cut Greece's debt to a level below 124 per cent of gross domestic product by 2020, officials said, though details were unclear early Tuesday morning (Europe time) after hours of contentious negotiations.

The deal should allow Greece to receive long-delayed loan payments of about €44 billion ($55bn) officials said will be paid in three installments. The agreement gets Greece's debt close to, but above, 120 per cent — the level beneath which the IMF has said it should fall by 2020 if the country is to nurse itself back to economic health.

European Central Bank President Mario Draghi Tuesday gave his blessing to a deal struck by Greece and its creditors that will have the country's aid program continue for the foreseeable future. "The ECB welcomes the deal," Mr Draghi told reporters as he left the building. "It will reduce uncertainty, and increase confidence in Europe."

Earlier, before details of the agreement emerged, the IMF expressed concerns even the 120 per cent mark is too high, according to one person familiar with the talks. "Everybody knows that even 120 per cent is too large for Greece," this person said, adding unsustainable debt would suppress outside investment and domestic demand. The IMF is responsible for around one-fifth of the €245.7bn in bailout money that has so far been promised to Athens. But it has said it can't continue funding Greece if there is no realistic prospect of the country eventually being able to finance itself again.

Because of that, the IMF was on Monday aiming for a two-pronged deal on Greece's bailout: It sought to have the eurozone take concrete measures now that would take Greece's debt load to close to 120 per cent of GDP by 2020, arguing without more action debt would remain above 140 per cent. At the same time, it was seeking a credible commitment from the eurozone to provide further debt relief once Athens has proved it can implement promised budget cuts and policy overhauls. "What we are looking for is measures upfront with credible promises down the road," the person familiar with the talks said Monday.

That demand signals issues with the country that first asked for an international bailout two and a half years ago are far from over. The currency union is already struggling to come up with measures that would reduce Greece's debt by decade's end, despite weeks of talks.

When they arrived in Brussels earlier in the day, most ministers had appeared optimistic. "We have entered here, the Europeans, with an accord practically agreed," said French Finance Minister Pierre Moscovici. According to officials, eurozone governments had been ready to lower the interest rates they charge Athens, redistribute profits they expect to collect from Greek bonds held by the European Central Bank and give the country more time to repay its debts, among other measures. But those plans would fall short of reaching the 120 per cent target by 2020, the officials said, leaving a deeper reduction even further out of reach.

In comments made as they arrived, ministers ruled out writing down the value of their bailout loans for Greece, with some arguing doing so would break their national laws. "All the members of the eurozone said two weeks ago that they're not in a position, as regards their own legislation, to accept a haircut if at the same time they have to give new guarantees," said Wolfgang Schäuble, Germany's finance minister.

However, one of the people said the IMF was willing to accept measures that would fall short of an actual write-down of the principal of eurozone rescue loans. Effective debt relief could also be achieved by cutting interest rates on bailout loans below funding costs and pushing loan maturities far enough into the future, he added.